Annual Compliance Calendar

BACKGROUND:

In this note, the note begins by referring to the provisions of the LLP Act, 2018 read with all the Amendment Acts and rules mentioned there till March 2025.

Post-incorporation requirements are duties that an LLP is required to meet after its incorporation. These include filing yearly reports, financial statements, changing Partners/Designated Partners, adjusting Contribution, and changing registered office.

All limited liability partnerships must keep annual accounts that show a true and fair picture of their financial situation. Even if the LLP does not do business, it must comply with statutory requirements such as the Annual Return, Balance Sheet, Profit and Loss Account, and Income Tax Return each year. The statutory fees will be based on the LLP’s capital contribution.

1. Financial Year of LLP:

Every LLP has to maintain uniform Financial ending on 31st March of the year. However, in case of LLP is incorporated after the 30th day of September of a year, the financial year may end on 31st March of the year next following that year.

Regular Works of LLP -LLP ACT- 2008:-

2. Annual e-Forms:

| S. No. | Agenda | Particulars | e-forms | Due Date Form Filling |

| 1. | Annual Return | Every LLP would be required to file annual return in Form 11 with ROC within 60 days of closer of financial year. | LLP-11 | 30th May |

| 2. | Statement Of Account & Solvency | A “Statement of Accounts and Solvency” in prescribed form shall be filed by every LLP with the Registrar every year. sub-section (3) of section 34 | LLP-8 | 30th October |

3. More about Form- 8 and 11:

What is Form – 11?

Form- LLP-11 is Annual Return containing number of partners, total contribution received by all partners, details of partners, detail of body corporates as partner, summary of partners.

Every LLP would be required to file annual return in Form 11 with ROC within 60 days of closer of financial year.

Due Date of Filling of LLP-11 30th May for each year.

What is Form – 8?

It is declaration given by all the designated partners of LLP that whether they are able to pay its debts in full as they become due in the normal course of business or not.

For the purposes of sub-section (3) of section 34, every limited liability partnership shall file the Statement of Account and Solvency in Form 8 with the Registrar, within a period of thirty days from the end of six months of the financial year to which the Statement of Account and Solvency relates.

Content of Form 8

Part A- Statement of Solvency

Part- B- Statement of Account, Statement of Income & Expenditure

Form- 8 is to be signed by two Designated Partners and certified by CS, CA, and CWA (in Whole Time Practice).

REGULAR OTHER REQUIREMENTS:

4. Requirement of Audit of Account Under LLP Act- 2008 (Rule 24) of LLP Rules – 2009.

where the partners of such LLP do not decide for audit of the accounts of the LLP, such LLP shall include in the Statement of Account and Solvency a statement by the partners to the effect that the partners acknowledge their responsibilities for complying with the requirements of the Act and the Rules with respect to preparation of books of account and a certificate in the form specified in Form 8.

Quick Bites:

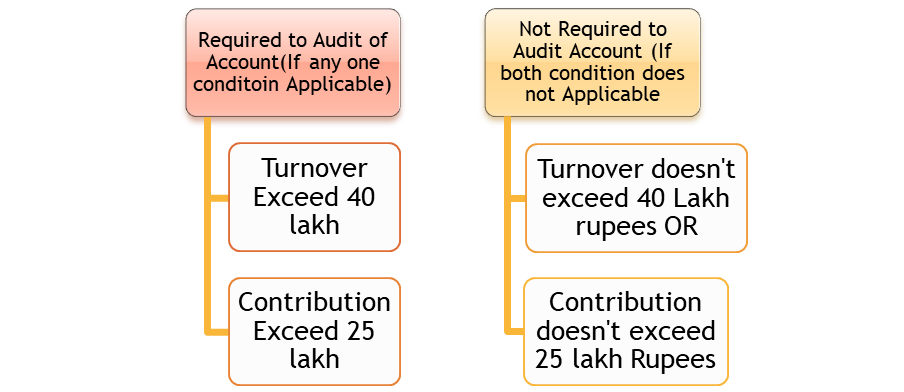

a) Is audit mandatory for LLP?

Audit of LLP is not mandatory. However, audit of LLP is mandatory if fulfil any of following conditions:

· Its turnover exceeds Rs. 40 Lacs; or

· Its contribution exceeds Rs. 25 Lacs.

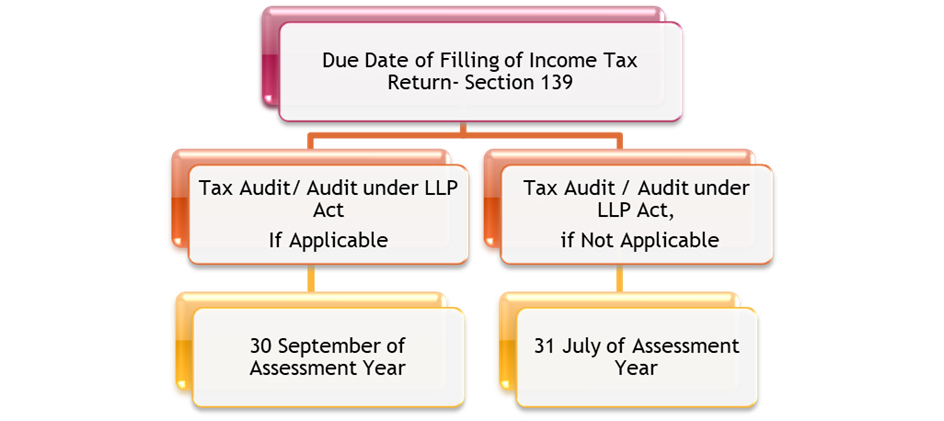

5. INCOME TAX RETURN:

Every LLP have to file the Income Tax return with the Income Tax Authorities. Filing of returns is mandatory whether the LLP has started any business or not. Date of Filling of Income Tax Return is as given below:

6. APPLICABILITY OF TAX AUDIT ON LLP:

| Carrying on business | Carrying on profession |

| Total sales, turnover or gross receipts exceed Rs. 1 crore in the FY. If cash transactions are up to 5% of total gross receipts and payments, the threshold limit of turnover for tax audit is increased to Rs. 10 crores (w.e.f. FY 2020-21). | Total gross receipts exceed Rs. 50 lakh in the FY. |

RETURNS AND RECORD REQUIRED BY LLP:

| S. No. | Agenda | Particulars | e-forms |

| 1. | Books of Account | LLP should Maintain proper Books of Account. | N.A. |

| 2. | Minutes Book | Minute’s book should be maintained to record minutes of meeting of partner and managing/ executive Committee of partners. | N.A. |

| 3. | Change in Partner | Any change in partner and designated partner (admission, resignation, cessation, death, expulsion) should be filed electronically within 30 days of change. | Form- 4 |

| 4. | Supplementary LLP Agreement | Such admission and cessation will alter mutual right and duties of partner shall change. Hence, supplementary LLP Agreement will be required to file within 30 days of change. | From-3 |

| 5. | Change in Name | Any change in Name of LLP should be filed electronically within 30 days of change. | Form-5 |

| 6. | Change in Registered Office | Any change in place of registered office of LLP should be filed electronically within 30 days of change. | Form- 15 |

Disclaimer: The entire contents of this document have been prepared based on relevant provisions and as per the information existing at the time of the preparation. Although care has been taken to ensure the accuracy, completeness, and reliability of the information provided, I assume no responsibility, therefore. Users of this information are expected to refer to the relevant existing provisions of applicable Laws. The user of the information agrees that the information is not professional advice and is subject to change without notice. I assume no responsibility for the consequences of the use of such information.